Convincing Features

Assignment Type

Subject

Uploaded by Malaysia Assignment Help

Date

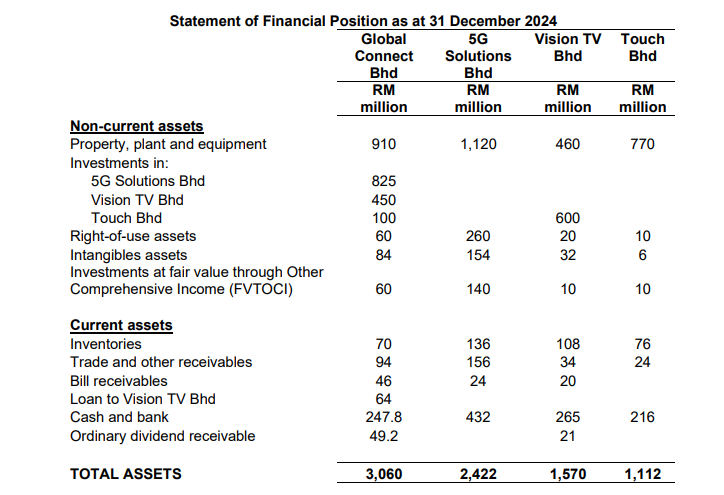

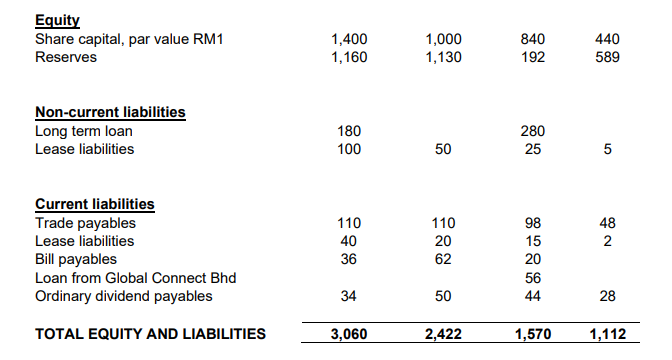

Global Connect Bhd is a leading provider of innovative communication solutions, dedicated to connecting people and businesses worldwide. Established in 2005, the company has been at the forefront of the telecommunications industry, offering a wide range of services including

mobile and fixed-line telephony, high-speed internet, and digital television. To achieve its goal of becoming the preferred telecommunications provider, Global Connect Bhd continuously innovates and adapts to meet the changing needs of its customers, strategically expanding through key acquisitions.

Investment in 5G Solutions Bhd

On 1 January 2021, Global Connect Bhd acquired 80% of the ordinary shares of 5G Solutions Bhd. On the date of acquisition, the retained profit and other reserves of 5G Solutions Bhd were RM250 million and RM50 million, respectively. The fair value of 5G Solutions Bhd’s net assets on the date of acquisition were equal to their carrying value. On 31 December 2023, the goodwill on the acquisition of 5G Solutions Bhd was impaired by 10%.

On 1 January 2024, Global Connect Bhd disposed half of its interest in the ordinary shares of 5G Solutions Bhd at RM4 per share. On that date, the fair value of 40% remaining interest in 5G Solutions were RM400 million. The disposal transaction has not yet been recorded.

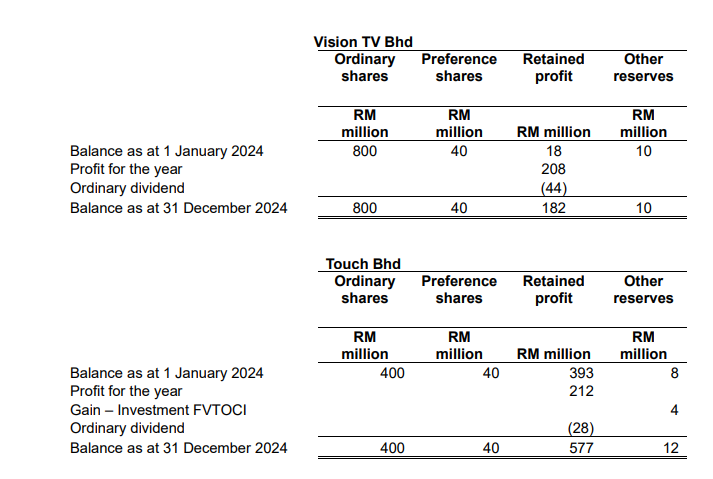

Investment in Vision TV Bhd

On 1 January 2024, Global Connect Bhd acquired 60% of the ordinary shares in Vision TV Bhd. The acquisition was settled on the following term:

a) An immediate cash payment of RM400 million.

b) A transfer of a building which has a carrying value of RM45 million. The fair value of the building was RM50 million.

c) RM0.20 cash for each share acquired payable on 1 January 2025. Global Connect Bhd has a cost of capital of 8%. The present value of the RM1 receivable in one year’s time is 0.926.

To date, only the cash payment and the building transfer have been recorded by Global Connect Bhd.

The fair value of Vision TV Bhd’s net assets on the date of acquisition were equal to their carrying amount. For the year ended 31 December 2024, goodwill on the acquisition of Vision TV Bhd was impaired by RM0.8 million.

Investment in Touch Bhd

On 1 July 2024, Vision TV Bhd and Global Connect Bhd acquired 300 million and 40 million of the ordinary shares of Touch Bhd, respectively. The fair value of the net assets of Touch Bhd were equal to their fair values except for:

a) Freehold land which had a fair value of RM3 million more than it carrying amount.

b) Internally generated brand which had a fair value of RM5 million with an indefinite useful life.

c) Contingent liability with an estimated fair value of RM0.5 million. This amount has not changed as at 31 December 2024.

Touch Bhd has not incorporated these fair value changes into its financial statements.

Significant Accounting Policies:

a) The non-controlling interest is measured at proportionate share method.

b) It is the group’s policy to provide depreciation for all assets using the straight-line method and full-year depreciation is to be provided in the year of purchase and none in the year of disposal. It is the policy of the company to record the depreciation and amortisation charged in the book of “General and Administrative expenses”.

c) All profits or losses are deemed to accrue evenly throughout the year unless otherwise specified.

Other Information:

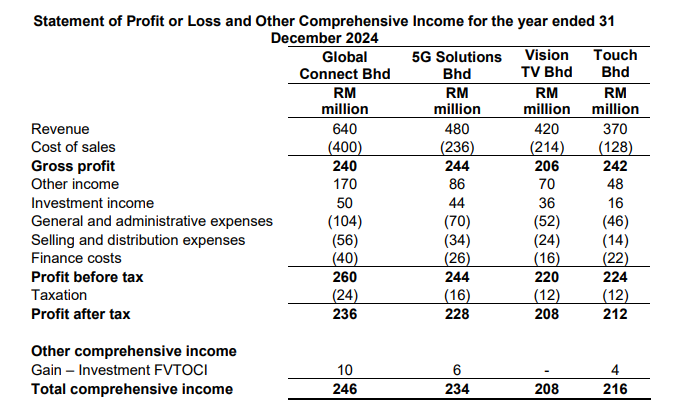

a) For the year ended 31 December 2024, Global Connect Bhd sold inventories to 5G Solutions Bhd for RM500,000 per month at a profit margin of 20%. Half of the goods remained in the inventory of 5G Solutions Bhd at 31 December 2024.

b) On 1 July 2024, Vision TV Bhd sold a specialised equipment to Global Connect Bhd at a profit of RM500,000. The specialised equipment had a remaining useful life of 5 years. Vision TV Bhd has recorded the profit on disposal in other income.

c) During the year, Global Connect Bhd and Vision TV Bhd purchased goods on credit worth RM100 million and RM70 million, respectively from Touch Bhd at a profit margin of 20%. A quarter of these goods are still in the inventories of Global Connect Bhd and Vision TV Bhd at the end of the year. As at 31 December 2024, Global Connect Bhd still owed Touch Bhd half of the goods purchased. Meanwhile, Vision TV Bhd has paid RM35 million for the goods purchased, but Touch Bhd only received RM30 million thereof, due to payment in transit.

d) On 31 December 2024, the investment at fair value through other comprehensive income of Vision TV Bhd had a fair value of RM10.5 million. This increase in value has not been incorporated in Vision TV’s account as at year end.

e) 5G Solutions Bhd, Vision TV Bhd and Touch Bhd had provided the final ordinary share dividend. The investors had recognised their shares from respective investees as investment income.

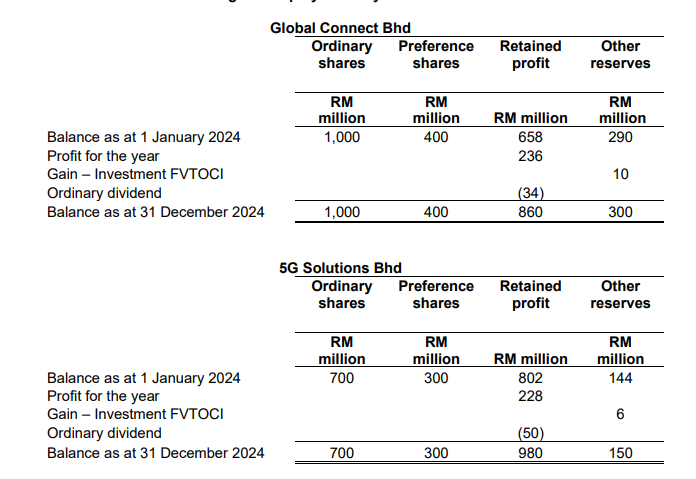

Statement of Changes in Equity for the year ended 31 December 2024

Required:

a. Compute goodwill or bargain purchase for the acquisition of 5G Solutions Bhd, Vision TV Bhd and Touch Bhd.

b. Compute the gain or loss on the disposal of 5G Solutions Bhd.

c. Compute the carrying amount of investment in 5G Solutions Bhd as at 31 December 2024.

d. Prepare the Consolidated Statement of Profit or Loss and Other Comprehensive Income of Global Connect Bhd Group for the year ended 31 December 2024.

e. Prepare Consolidated Statement of Changes in Equity of of Global Connect Bhd Group for the year ended 31 December 2024.

f. Prepare the Consolidated Statement of Financial Position of Global Connect Bhd as at 31 December 2024.

a. Prune Bhd holds 45% of the shares in Seaweed Sdn Bhd, while the remaining 55% is owned by several small investors who lack significant influence. Although Prune Bhd owns less than half of the shares, it has appointed three out of five board members and influenced key strategic decisions within Seaweed Sdn Bhd.

Based on MFRS 10, is Prune Bhd considered to have “control” over Seaweed Sdn Bhd?

b. Nyatoh Bhd acquired 30 million ordinary shares in Semangkok Bhd for RM100 million. The issued capital of Semangkok Bhd comprised 200 million ordinary shares. Nyatoh Bhd also has share options that allow it to acquire another 20 million shares in Semangkok Bhd. If Nyatoh Bhd exercises its rights, the enlarged share capital of Semangkok Bhd will be 220 million shares.

i. Discuss the accounting treatment of the investment in Nyatoh Bhd’s financial statement and consolidated financial statements.

ii. If the share options held by Nyatoh Bhd are not substantive, how investment in Semangkok Bhd shall be accounted in the books of Nyatoh Bhd.

c. Ranting Bhd, a publicly listed manufacturing company, has engaged Dahan Sdn Bhd, a private logistics company, to provide transportation and warehousing services for its goods. Puan Hawa, the CEO and a key member of Ranting Bhd’s management team, owns 25% of Dahan Sdn Bhd, while his brother, Mr. Adam, who serves as the Managing Director of Dahan Sdn Bhd, holds a 30% ownership stake.

Based on the scenario, identify the related parties to Ranting Bhd. Justify your answer.

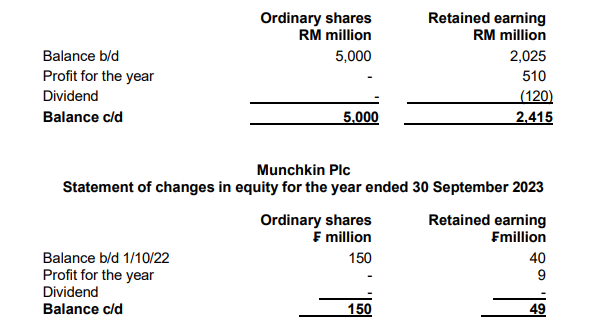

On 1 October 2022, Seraya Global Bhd, a Malaysian corporation, paid cash to acquire 75% of the ordinary shares of Munchkin Plc., an overseas subsidiary whose local currency is FHK (₣). The main business activity of Munchkin Plc is to manufacture products in Switzerland for the home market. Most transactions are made in FHK (₣), the local currency. Munchkin Plc’s

management has significant autonomy in running the business. Munchkin Plc does not rely on Seraya Global Bhd to finance its operations.

The following are the financial statements of Seraya Global Bhd and Munchkin Plc for the year ended 30 September 2023, measured in their functional currencies:

Statements of Profit or Loss and Other Comprehensive Income for the year ended 30 September 2023

Seraya Global Bhd

| RM million | |

|---|---|

| Revenue | 4,620 |

| Less: Cost of goods sold | (3,465) |

| Gross Profit | 1,155 |

| Less: Expenses | (425) |

| Profit before tax | 730 |

| Tax expense | (220) |

| Profit after tax | 510 |

| Other comprehensive income | |

| Surplus on revaluation | 180 |

| Total comprehensive income | 690 |

Munchkin Plc

| ₣ million | |

|---|---|

| Revenue | 296 |

| Less: Cost of goods sold | (222) |

| Gross Profit | 74 |

| Less: Expenses | (50) |

| Profit before tax | 24 |

| Tax expense | (15) |

| Profit after tax | 9 |

| Other comprehensive income | |

| Surplus on revaluation | – |

| Total comprehensive income | 9 |

Seraya Global Bhd

Statement of changes in equity for the year ended 30 September 2023

Statements of Financial Position as at 30 September 2023

Seraya Global Bhd

| RM million | |

|---|---|

| Non-Current Assets | |

| Property, Plant & Equipment | 5,150 |

| Quoted investment | 1,005 |

| Investment in Munchkin Plc | 700 |

| Inventories | 690 |

| Trade receivables | 420 |

| Cash and bank | 500 |

| Total | 8,465 |

| Ordinary shares | 5,000 |

| Retained earning | 2,415 |

| Asset revaluation reserve | 180 |

| Long term loan | 250 |

| Ordinary dividend payable | 120 |

| Trade payables | 500 |

| Total | 8,465 |

Munchkin Plc

| ₣ million | |

|---|---|

| Non-Current Assets | |

| Property, Plant & Equipment | 115 |

| Quoted investment | 63 |

| Investment in Munchkin Plc | – |

| Inventories | 31 |

| Trade receivables | 23 |

| Cash and bank | 26 |

| Total | 258 |

| Ordinary shares | 150 |

| Retained earning | 49 |

| Asset revaluation reserve | – |

| Long term loan | 30 |

| Ordinary dividend payable | – |

| Trade payables | 29 |

| Total | 258 |

Additional Information:

Required:

Note: Show all workings to the nearest RM Million with two decimal points.