Convincing Features

School

*We aren't endorsed by this school

Assignment Type

Subject

Uploaded by Malaysia Assignment Help

Date

NQK Eco Packaging Berhad is a company operating in the Corrugated Boxes Manufacturing sector. Corrugated boxes are popular because of their strength, durability, lightness, recyclability, and cost-effectiveness. The packaging materials are manufactured based on the latest technology with sufficient verification and testing.

The company was incorporated in Malaysia with nominal capital of RM7,000,000 comprising of 2,500,000 units of ordinary shares of RM2.20 each and the remaining capital is 7% redeemable preference shares of RM1.50 each.

The following is the trial balance of NQK Eco Packaging Berhad as at 31 December 2024:

| DEBIT | RM | CREDIT | RM |

|---|---|---|---|

| Turnover | 7,300,000 | ||

| Cost of sales | 1,697,250 | ||

| Selling and distribution costs | 372,500 | ||

| Administrative expense | 156,250 | ||

| Interim ordinary dividend | 257,500 | ||

| Interim redeemable preference dividend | 52,500 | ||

| Interest on debentures | 13,650 | ||

| Tax paid | 339,000 | ||

| Inventories as at 31 December 2024 (cost) | 150,000 | ||

| Accounts Receivable and Accounts Payable | 195,200 | 162,500 | |

| Bank | 10,766,000 | ||

| 7% Debentures | 390,000 | ||

| Ordinary share capital | 5,500,000 | ||

| 7% Redeemable Preference shares capital | 1,500,000 | ||

| Retained profit as at 1 January 2024 | 782,500 | ||

| Allowance for impairment of trade receivables (at 1 January 2024) | 21,675 | ||

| Freehold land | 750,000 | ||

| Building (at cost) | 450,000 | ||

| Plant and Machinery (at cost) | 472,500 | ||

| Motor Vehicles (at cost) | 381,250 | ||

| Accumulated Depreciation at 1 January 2024 | |||

| Building | 72,000 | ||

| Plant and Machinery | 212,625 | ||

| Motor vehicles | 186,050 | ||

| Directors’ remuneration | 73,750 | ||

| Total | 16,127,350 | 16,127,350 |

As at 31 December 2024, the following information has not been included in the company’s financial statements:

1. The information related to the property, plant, and equipment of the company is as follows:

a. The land was revalued to RM825,000. The directors decided to incorporate the new value in its book. The depreciation policy of the company is as follows:

I. Building over its useful life of 50 years

ii. Plant and Machinery 15% per annum on cost, yearly basis

iii. Motor vehicles 20% on net carrying amount, monthly basis

Note: Depreciation on motor vehicles is treated as selling and distribution expenses while depreciation for other property, plant and equipment is treated as administrative expenses.

b. Due to the business expansion plan, NQK Eco Packaging Berhad has decided to purchase an Automatic Corrugated Box Making Machine. On 1 August 2024, the company purchased an Automatic Corrugated Box Making Machine Model FF 2800 from India. This machine is expected to be used for 10 years. Below are the costs incurred on acquisition of this machine Model FF 2800:

| Invoice price | 375,000 |

| Insurance on shipping | 1,450 |

| Installation & assembly cost | 1,850 |

| Cost of staff training | 750 |

| Staff’s salaries | 1,670 |

| Import duty | 950 |

| Trade discount | -2% |

The payment for the automatic machine was made by cheque. No record was made for this transaction.

c. The current growth of various industries has given rise to incease in demand forcorrugated boxes for product packaging and transportation. As a consequence, thecompany had acquired additional truck on 23 March 2024 in order to meet theincrease in demand. The truck was purchased on credit. The costs incurred were as follows:

| Description | Amount (RM) |

|---|---|

| Purchase price | 180,000 |

| Trade discount | 5% |

| Road tax & insurance | 2,700 |

| Cost of painting company’s logo | 1,900 |

On 23 September 2024, one of the truck costing RM39,000 involved in an accident and totally damaged. The management has decided to write off the truck from the company’s books. Company received RM11,000 from the insurance company as compensation. The vehicle was acquired on 9 July 2022.

a. Explain whether an automatic corrugated box making machine can be classified as an item of property, plant, and equipment in accordance with MFRS 116 Property, Plant, and Equipment. (3 marks)

b. Compute the initial cost for all the assets acquired by the company during the year. (4 marks)

c. Calculate the accumulated depreciation for the disposed truck. (4 marks)

d. Recommend the company on the accounting treatment on derecognition of the disposed truck. (5 marks)

e. Advise the accounting treatment and the journal entries for the revaluation of land on 31 December 2024. (4 marks)

2. The company uses a group of similar items basis in valuing its inventories. As at 31 December 2024, the following types of corrugated boxes remained unsold:

| Inventory Items | Purchase Price (RM) | Selling Price (RM) |

|---|---|---|

| Slotted boxes – 3 ply | 12,500 | 11,250 |

| Slotted boxes – 5 ply | 10,000 | 12,000 |

| Slotted boxes – 7 ply | 27,500 | 26,250 |

| Self-Erecting boxes – 3 ply | 30,000 | 32,500 |

| Self-Erecting boxes – 5 ply | 15,000 | 17,500 |

| Self-Erecting boxes – 7 ply | 20,000 | 21,250 |

| Folder boxes – 3 ply | 18,750 | 17,000 |

| Folder boxes – 5 ply | 8,750 | 8,500 |

| Folder boxes – 7 ply | 7,500 | 7,000 |

Required:

I. MFRS102 Inventories requires that inventories shall be measured at the lower of cost and net realizable value. Explain the importance of this rule in accounting practice. (3 marks)

ii. Explain the value of closing inventory that will be disclosed in the Statement of Financial Position as at 31 December 2024. (show all workings) (5 marks)

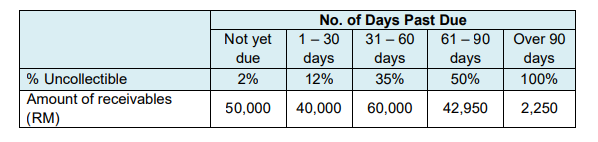

3. The company’s aging analysis of receivables as at 31 December 2024 is as follows:

Required:

I. Compute the amount of allowance for impairment of trade receivables to be disclosed in the statement of financial position for the year ended 31 December 2024. (show all workings) (4 marks)

ii. Determine net realizable value of trade receivables as at 31 December 2024. (2 marks)

4. On 14 September 2024, NQK Eco Packaging Berhad ordered 5 tons of high-quality kraft paper liner board from Golden Paper Berhad worth RM68,400. Two days later, Golden Paper Berhad delivered kraft paper liner board with an invoice of RM68,400. Additional costs include transportation cost of RM1,300, insurance on purchase of RM2,200, and storage costs of RM1,800. The storage costs were recorded as administrative expenses during the year.

On 23 September 2024, the company paid half of the outstanding debt to Golden Paper Berhad by cheque and received a discount of 10% from the supplier. On 21 December 2024, the company paid the remaining balance to Golden Paper Berhad by issuing a cheque.

I. Prepare the journal entry to record the payment made on 23 September 2024. (3 marks)

ii. Discuss whether NQK Packaging Solution Berhad can derecognize Golden Paper Berhad from the company’s book on 31 December 2024. (3 marks)

5. During the year, the directors proposed the following:

I. Transfer to general reserve of RM80,000.

ii. Final dividend for redeemable preference shares and final dividend of 20

sen per share for ordinary shares.

iii. Rights issue of 1 for every 10 ordinary shares held with a price of RM2.00 per share to its existing shareholders. The shares were fully subscribed and paid. The rights issue shares do not rank for final dividends.

6. As at 31 December 2024, the following amount were outstanding:

i. Auditor’s fees of RM10,000

ii. 6 months’ interest on debentures

7. Tax expense for the year was RM305,000

Considering the adjustments from No.1-7 and in compliance with Companies Act 2016, MFRS101 Presentation of Financial Statements and other relevant Malaysian Financial Reporting Standards:

a. Prepare the Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2024. (28 marks)

b. Present the Statement of Changes in Equity for the year ended 31 December 2024. (7 marks)

c. Determine the Statement of Financial Position as at 31 December 2024. (12 marks)

d. Prepare the notes on property, plant, and equipment. (5 marks)