BFW3121: The table below depict the expected return CCC Berhad and XXX Berhad for April and May:: Investments and portfolio management Coursework, MUM, Malaysia

Assignment Type

Individual Assignment

Subject

BFW3121: Investments and portfolio management

Uploaded by Malaysia Assignment Help

Date

08/02/2022

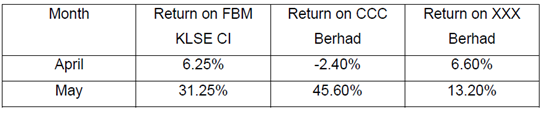

The table below depict the expected return CCC Berhad and XXX Berhad for April and May:

a) Calculate the betas for both stocks.

b) Discuss the problems encounters when testing the CAPM empirically.

c) In light of the problems in CAPM: the APT model was proposed as an alternative. Discuss how the APT overcome the shortcoming of CAPM.

Suppose there are an infinite number of assets with an expected return of 12% p.a. and a standard deviation of 40%. Further, assume investors form equally-weighted portfolios.

(a) If the correlation between any two assets is zero, calculate the expected return and standard deviation of a randomly selected two-stock portfolio and three-stock portfolio.

(b) If the correlation between any two assets is 0.45. elaborate the highest possible expected return and lowest possible standard deviation in this case.

(c) Explain the implications of your results to the concept of diversification based on the key differences between the two approaches in estimating the mean variance optimal portfolio: the Sharpe diagonal and the Markowitz approach.

Get 30% Discount on This Assignment Answer Today!

Get Help By Expert

Get top quality coursework writing help on BFW3121: Investments and portfolio management by malaysia Assignment Help. Our experts have phd and master degree in their subject field. also our writers are ready to provide step by step guidance on management assignment at a cheap price.

Recommended Assignments for You

Related University Assignments

- ACW1020 Accounting in Business Assignment 2, 2026 | Monash University

- MKW3000 Strategic Branding Assignment 2 Brief 2026 | Monash University

- MKW1120 Marketing Fundamentals Assignment 1 Brief 2026 | MUM

- ETW3420 Principles of Forecasting and Applications Individual Assignment 3, Monash University Malaysia

- Principle of Macroeconomics Group Assignment September 2025

- Alternative Dispute Resolution Assignment: Addressing Consumer Disputes, Contract Clauses, and Employee Rights

- Macroeconomic Growth Assignment: OLS Time-Series Analysis Using 2015–2025 Economic Data

- 3D Point Cloud Segmentation Assignment: Oil Palm Tree Classification Using ML Techniques

- Heat Sink Design Assignment Project: Thermal Optimization for T/R Module in Phased Array Antenna

- International Business Analysis Assignment Report: MNC Operations, Trade Theories & Environmental Challenges in North America and Asia

Convincing Features